Cloud Expending To Leading $1 Trillion In Four Several years

There is some uncertainty about global IT paying in the broadest feeling in 2023 and past, and but Synergy Study, which watches the cloud section like a hawk, is quite bullish on cloud expending in its many guises.

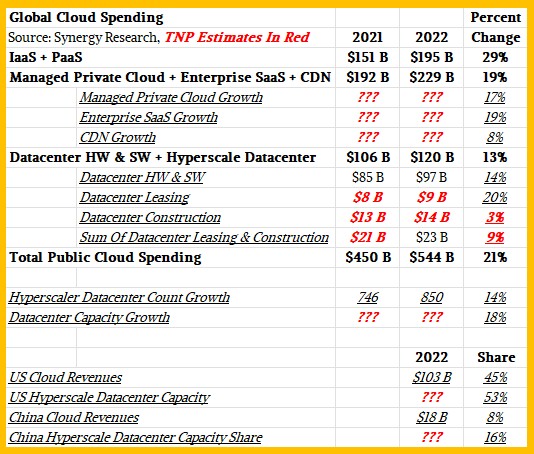

In truth, the organization reckons that across the cloud solutions and infrastructure sectors. Total paying out revenues for cloud operators and hardware, application, and solutions sellers – what it phone calls the community cloud ecosystem – rose by 21 per cent in 2022 to reach $544 billion, and states additional in its forecast that product sales across that cloud ecosystem will double to in excess of $1 trillion in the upcoming four many years.

Doubling would mean $1.09 trillion in sales. That is a compound yearly advancement price of 26 p.c over all those 4 decades, and simply because Dinsdale is not at liberty to say what the 2023 projection is – Synergy Investigate has to make a living, as well – we have to presume this 26 percent CAGR as a proxy for 2023’s advancement.

As we documented by in October, Gartner has cased what it calls “Datacenter System” profits at $189.5 billion in 2021, escalating by 10.4 percent to $209.2 billion in 2022 with a projected – and decelerating – progress of 3.4 percent to $216.3 billion in 2023. If you add in application and IT companies to get a proxy for main IT paying, then Gartner believes that this main IT shelling out rose by 12.8 per cent to $2.13 trillion in 2021. And possibly a lot more considerably, Gartner is only projecting 6 per cent progress in that core IT shelling out variety to $2.26 billion in 2022 and says further more that development will be 8.7 p.c in 2023 to $2.45 trillion – with advancement driven pretty much entirely by an improve in organization software package shelling out.

What is obvious by comparing these two datasets is that the cloud ecosystem is expanding more rapidly than IT total and seems to be to continue to do so in the 12 months forward and incredibly very likely beyond.

Apparently, Synergy Exploration says that the selection of “operational hyperscale datacenters” would improve by only 50 p.c around that time. John Dinsdale, chief analyst and exploration director at Synergy Study, provides that datacenter community ability will maximize by about 65 p.c over the following four a long time.

Counting “hyperscale” datacenters – not cloud regions, but the self-contained datacenters with a one network connected all of their equipment into one substantial virtualized equipment that in convert comprise a cloud area – is fascinating. But you have to always keep in mind that some of these datacenters are for internally formulated programs at what we at The Subsequent Platform phone “hyperscalers” that operate on their infrastructure but cloud hardware underpinning it is a expense of products offered. Some hyperscalers are not in the cloud business at all, like Facebook in the United States and ByteDance in China (which has a couple of dozen programs including TikTok). In the United States, Google, Microsoft, and even AWS have software and storage products and services that are really finest labeled as SaaS, and ditto for Alibaba, Baidu, and Tencent. We provide this up not to pick, but to stage out that when we say “hyperscale” we suggest a really exact thing – it indicates all those apps that are absolutely free or affordable and the iron and application that comprise it. We do not necessarily mean cloud, which signifies capability in some type for hire.

“We observe this pretty intently,” Dinsdale suggests of the hyperscale datacenter figure in speaking to The Upcoming System. “In December the quantity of operational hyperscale datacenters passed the 850 mark. The quantities is escalating by ~100 per 12 months. These are all huge datacenters and exclude CDN nodes, compact regional POPs, and rather small edge deployments. It also excludes all datacenters that are in the pipeline (becoming planned, created or quickly to be launched). That provides a further 420 datacenters.”

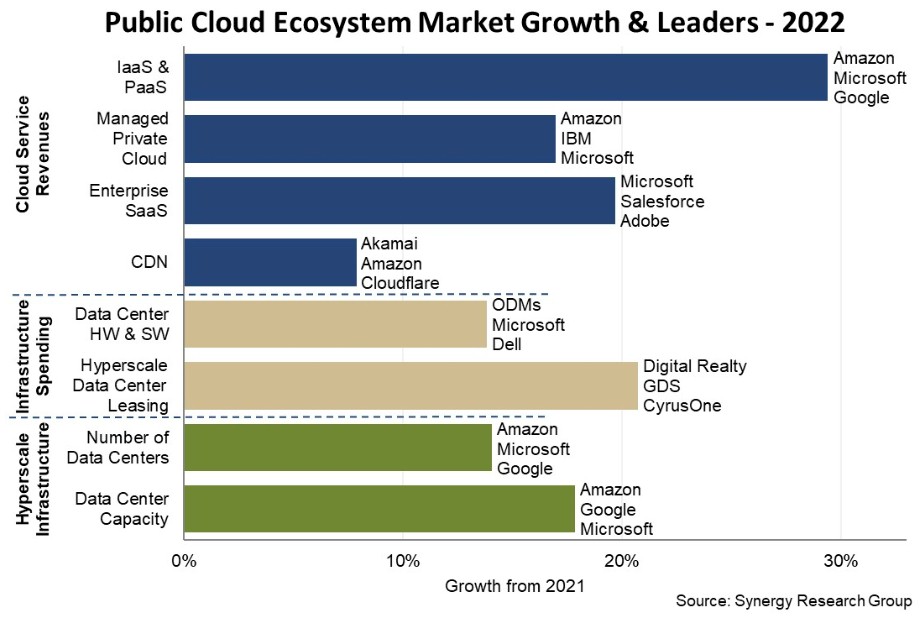

Listed here is the chart that Synergy Exploration place out casing the community cloud ecosystem in 2022:

We really don’t use the word “public” to converse about clouds any longer, given that there is practically nothing general public about this. Cloud are indeed utilities, but they absolutely sure as hell are not regulated like other public utilities governing the distribution of electric power, natural gas, or drinking water most surely are.

The chart higher than demonstrates development prices, not revenues, so be watchful when you look at it. We appeared at the couple figures in the Synergy Exploration executive summary and other opinions that Dinsdale produced to us and cooked up this desk that gives you the earnings degrees as nicely as the progress fees of the info place out by Synergy Exploration:

To get the development rates for the chart, we printed out the chart and calculated the bars, and the moment we experienced that, we could figure out the revenues for 2021 for certain parts of the Synergy Exploration details. Dinsdale informed us that The $120 billion in datacenter hardware and software program marketed for clouds and hyperscalers in 2022, 81 % was for components and software acquired and 19 per cent was for datacenter leasing (both of those equipment and services) and for building of physical datacenters.

We did not have ample info to figure out how significantly was for datacenter leasing and how much was for building, but if you make one assumption you can calculate all of the lacking facts under the datacenter. What we know is that the Datacenter Building bar, which is lacking from the Synergy Investigation chart, have to have been incredibly modestly developing or down for the total category to only expand by 13 per cent when two of the subsegments grew by 14 percent and 20 p.c as calculated from the bar chart. The figures proven in bold red italics are out estimates dependent on a 40-60 break up concerning datacenter leasing and datacenter building in 2022.

We are not confident adequate of the Managed Private Cloud, Company SaaS, and CDN segments to make estimates, but we have revealed the expansion costs from the bar chart.

As you can see, this “public cloud ecosystem” dataset mixes datacenter components and computer software expending by clouds with conclude consumer paying out on clouds, and we can discussion the knowledge of that. But obtaining the info damaged out individually, as Synergy Study presents it, means we can tear it apart. To our way of imagining, the spending on datacenter capability is a price of products bought for the genuine cloud IaaS and PaaS services that are offered. And likewise, SaaS sellers that runs their applications on just one or much more of the clouds has an IaaS or PaaS assistance as a charge of goods marketed for their SaaS offerings.

Synergy gives a breakdown of cloud revenues and cloud capacity for the United States and China, and as you can see from the table, the United States completely dwarfs China in phrases of revenues. We never know the capacities of these datacenters – expressed as megawatts of crucial IT load – because Dinsdale is keeping that to himself, but we do know that the US stands at 53 percent of megawatts compared to 16 p.c for China.